“Market participants willing to accept illiquidity achieve a significant edge in seeking high risk-adjusted returns. Because market players routinely overpay for liquidity, serious investors benefit by avoiding overpriced liquid securities and by embracing less liquid alternatives.” ― David F. Swensen, Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment, Fully Revised and Updated

Over the Summer, the markets soared to new highs, erasing the effects of the global pandemic, as investors seemed complacent about the inherent risks. The market’s rise was fueled by accommodative Fed policy and a flood of Fiscal and Monetary stimulus. Recently however, volatility and uncertainty have reemerged.

There are substantial risks that may cause a major set-back in the not too distant future including: elevated valuations, uncertainty surrounding reopening the economy, increasing COVID cases, social unrest, and a volatile election season. Any of these events could cause a pull-back, or worse yet a recession.

During the bull-market, many advisors shied-away from allocating to alternative investments. I have suggested that there have been a number of factors contributing to the relatively low allocation to alternatives across the wealth management industry, including the terminology used with advisors and investors, a lack of education regarding the role and use of alternatives, and establishing realistic performance expectations.

The terminology has been confusing for both advisors and investors. Investors are often confused about strategy versus structure. They think that alternatives are a homogenous group with all strategies seeking the same outcome. Of course, alternative investments represent a broad array of strategies which are typically structured in a limited partnership structure[i]. Global Macro is vastly different from Event-Driven in their approach; and Alternative Credit and Managed Futures deliver wildly different results over time.

These strategies are often referred to broadly as hedge funds. In recent years, many of these strategies have been packaged in a mutual fund structure (i.e., liquid alternatives). Liquid alternatives address some of the structural limitations of hedge funds - lack of transparency, lack of liquidity and high fees – but the jury’s still out regarding whether they deliver comparable results.

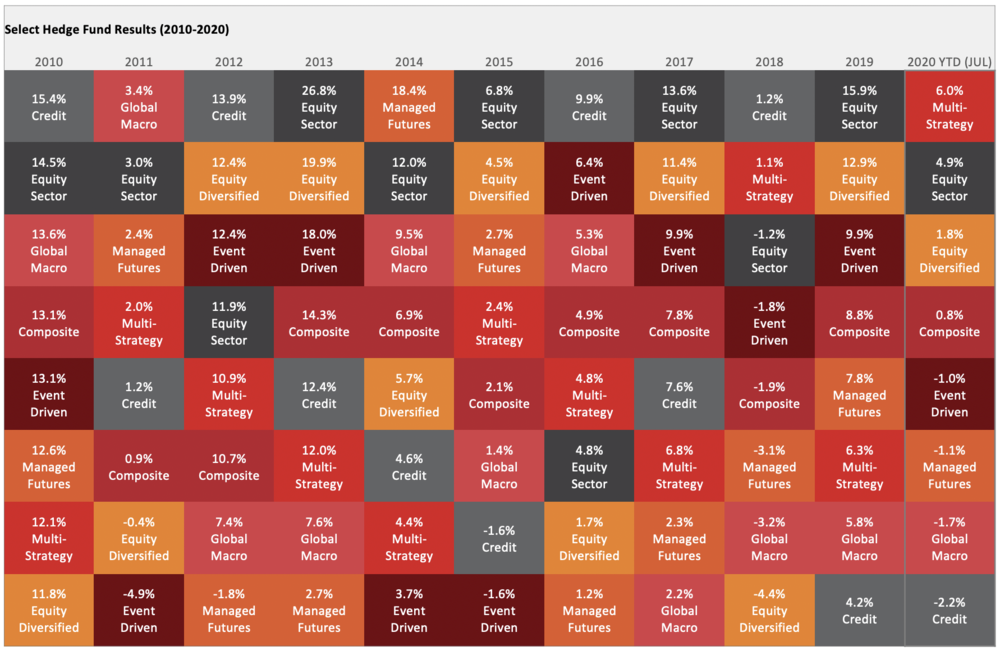

To illustrate the differences amongst these strategies, please see the results below highlighting the best and worst performing strategies over time. Credit strategies were the top performers in 2010, 2012, 2016 and 2018 – and the bottom performers in 2019 and 2020. Credit strategies include Convertible Arbitrage, Distressed and Long/Short Credit, among others.

Source: PivotalPath Data through 8/17/2020

Source: PivotalPath Data through 8/17/2020

The chart above depicts the performance of PivotalPath's Hedge Fund Indices, ranked from best to worst. Each strategy is color-coded for easy tracking. For additional information, visit pivotalpath.com.

Equity Sector has generally been one of the top performers, with healthcare, technology, media, and telecom generating strong results; and financials, energy and utilities lagging over time. Multi-Strategy has been the best strategy year-to-date.

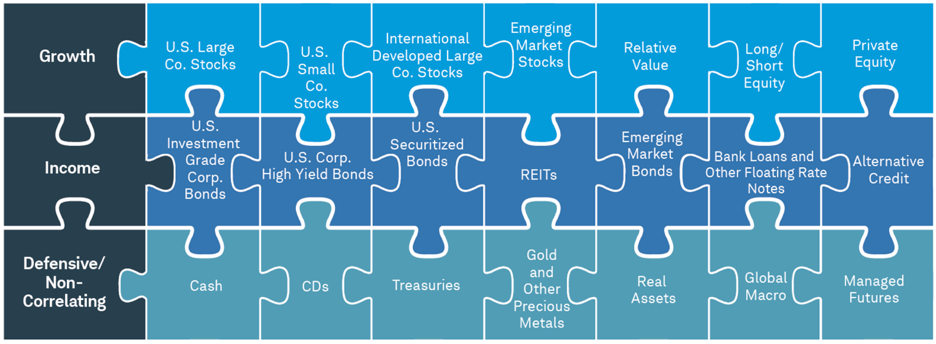

Like the way that we view the natural rotation of traditional asset class results over time, we need to view alternatives as distinct investments, each solving for a specific portfolio need over time. Relative Value and Long / Short Equity are growth-oriented strategies, Alternative Credit helps in generating income, and Global Macro and Managed Futures are more defensive strategies[ii]

With recent market volatility, advisors may want to revisit their alternative allocations. There are significant risks that may lead to a correction in the coming months. Advisors may want to consider alternative investments as potential sources of returns and income – and to dampen portfolio volatility.

Advisors should take the lead in educating investors about the merits of alternative investments and the vital role they play in building durable portfolios.

Sources:

[i] Davidow, Anthony, “Alternative Investments: A Goals-Based Framework”, Investments & Wealth Monitor, November-December 2018

[ii] Davidow, Anthony, “Democratizing Alternative Investments”, Investments & Wealth Monitor, March-April 2016